Data Note

The Pension Trade: How Kenya's Retirement Money Became a Government Bond Fund

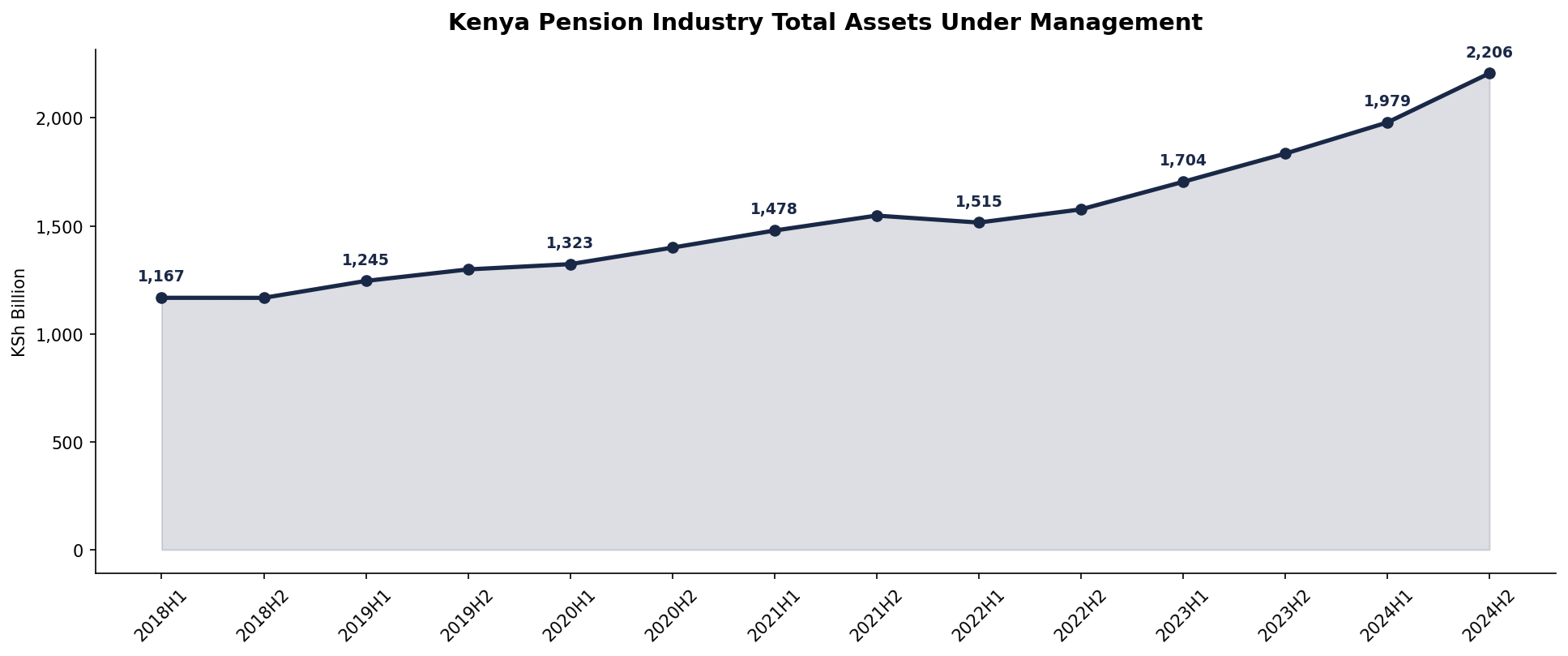

Between 2018 and 2024 the Kenyan pension industry nearly doubled in size, growing from KSh 1.17 trillion to KSh 2.21 trillion. But the composition of that growth tells a story regulators, savers, and the National Treasury all need to take seriously: more than half of every pension shilling now sits in government securities.

The data

The Retirement Benefits Authority publishes semi-annual data on the asset allocation of the Kenyan pension industry. We analysed seven years of it, from 2018 H1 through 2024 H2. Across that window the industry grew by KSh 1.04 trillion, accumulating new contributions and investment returns into a portfolio that now stands at KSh 2.21 trillion.

The headline number is healthy. The industry compounded at 10.3 percent a year, faster than nominal GDP and faster than wages. Pension contributions are working.

Where the money went is a different matter.

The two big winners

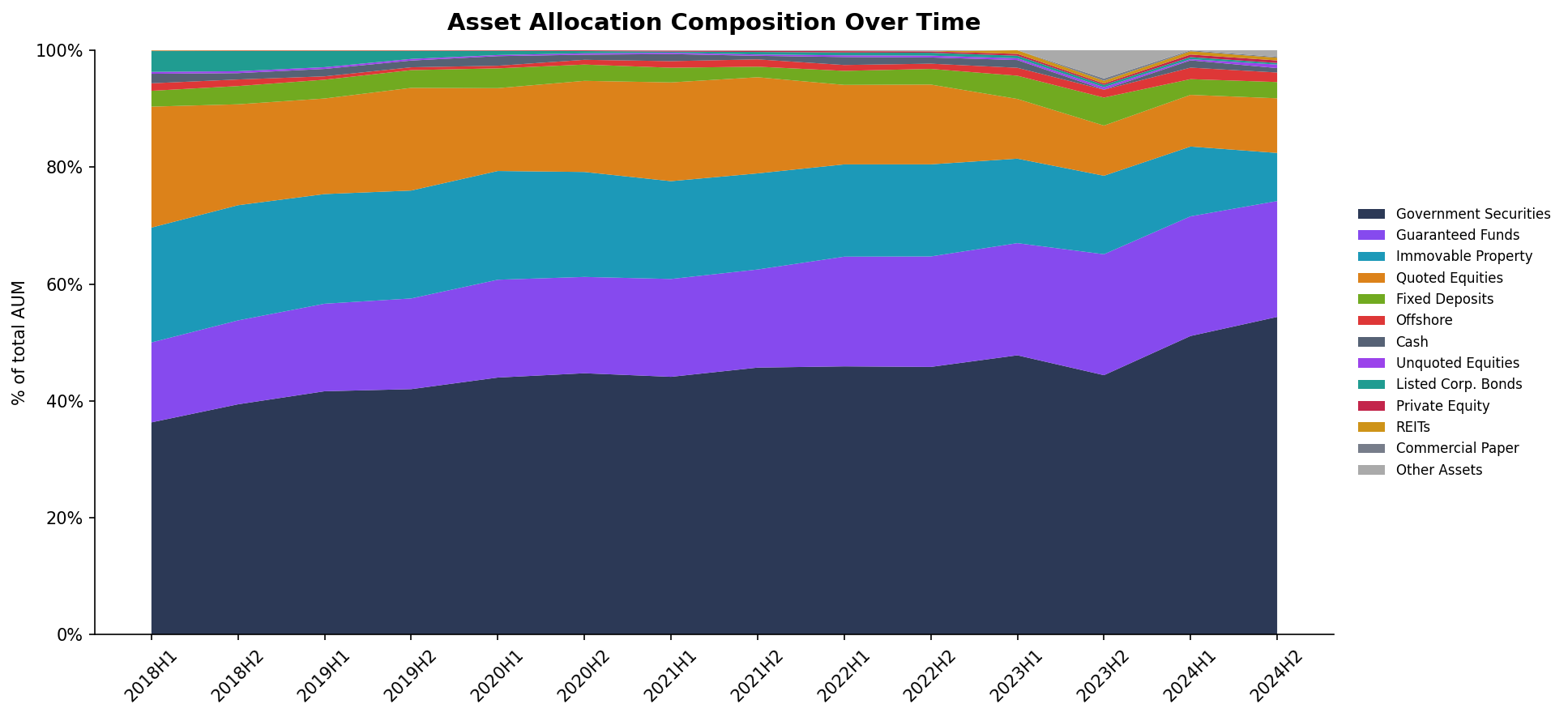

Government securities now make up 54.4 percent of the entire pension industry. In 2018 that figure was 36.3 percent. The absolute increase is even more striking. Pension holdings of Treasury bills and Treasury bonds rose from KSh 424 billion to KSh 1.20 trillion. Government paper grew by 183 percent in seven years, while the rest of the portfolio grew by 41 percent.

Put differently, of every shilling of new pension money raised between 2018 and 2024, roughly seventy five cents was deployed into government securities.

The second fastest growing asset class was guaranteed funds. These are insurance wrapped products in which the scheme transfers investment risk to an insurance company in exchange for a stated minimum return. Their share of total pension assets rose from 13.7 percent to 19.8 percent. In absolute terms guaranteed funds nearly tripled, from KSh 160 billion to KSh 438 billion.

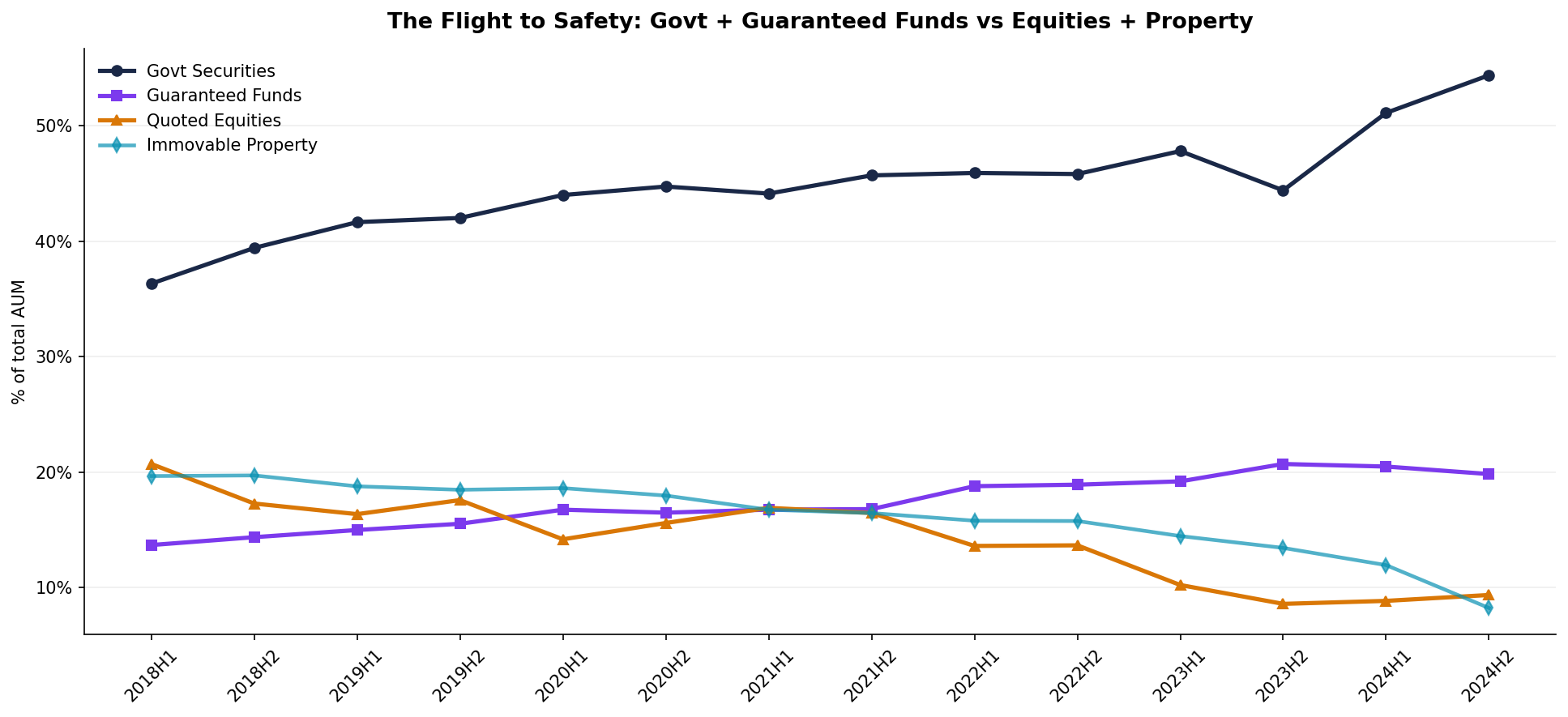

The pattern these two share is unmistakable. Both are low risk, low volatility, high credit quality assets. Pensions are de risking, and they are doing so with conviction.

The two big losers

Quoted equities fell from 20.7 percent of pension portfolios to 9.4 percent. The Nairobi Securities Exchange, the largest stock market in East Africa, now claims one in ten pension shillings, down from one in five.

The absolute number tells the same story. Pension holdings of NSE listed equities are smaller in 2024 (KSh 206 billion) than they were in 2018 (KSh 242 billion). This is despite the industry doubling in size. In real terms, pension funds have withdrawn from the NSE during a period when the index has been flat or declining and the shilling has weakened.

Immovable property fell almost identically hard, from 19.7 percent to 8.2 percent. Direct real estate holdings shrank in absolute terms, from KSh 229 billion to KSh 182 billion, even as the rest of the industry grew. There is no offsetting growth in real estate investment trusts to explain the shift; REITs remain a rounding error in Kenyan pension portfolios.

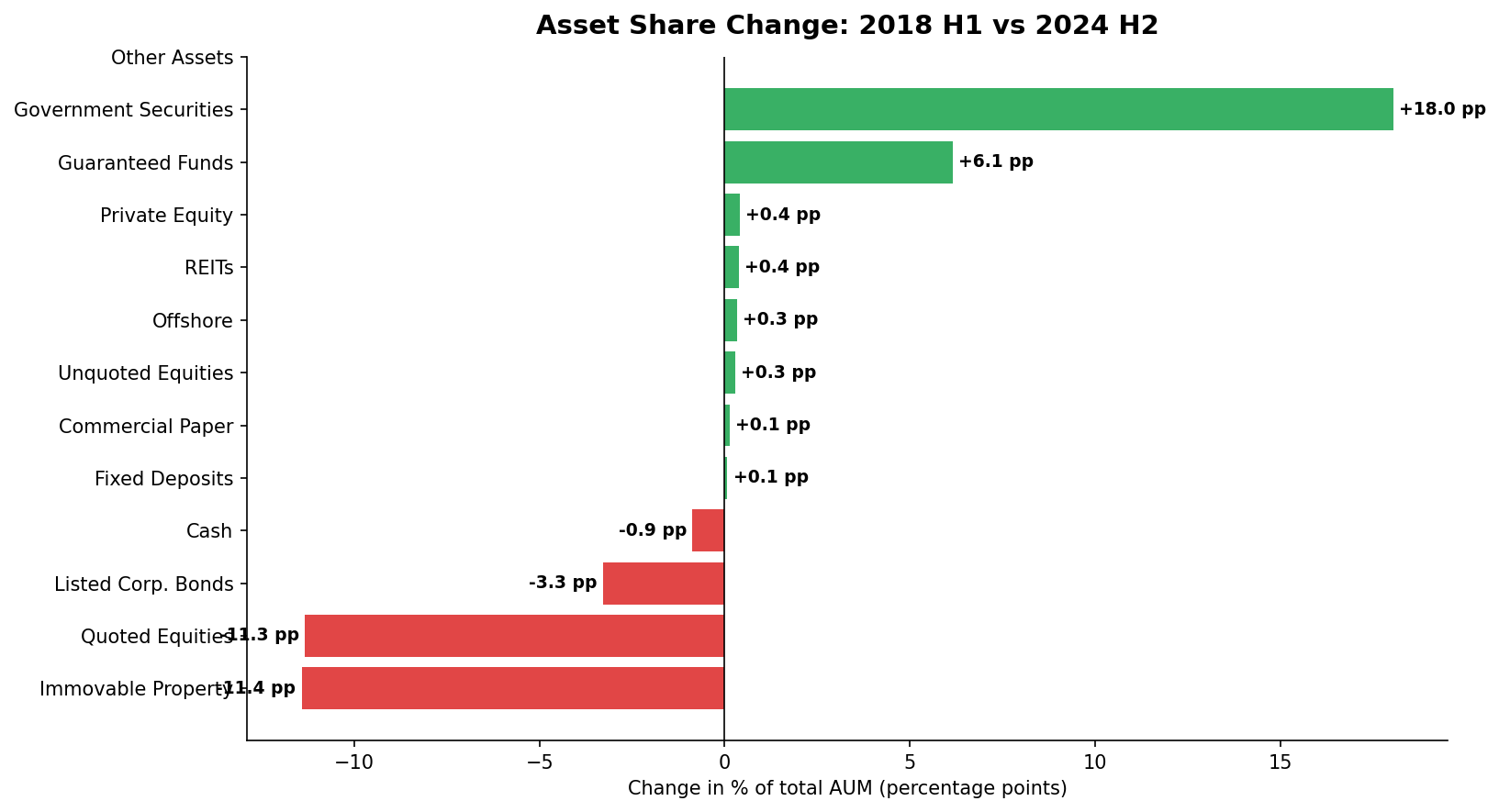

The composition shift, in one table

| Asset class | 2018 H1 share | 2024 H2 share | Change |

|---|---|---|---|

| Government Securities | 36.3% | 54.4% | +18.1 pp |

| Guaranteed Funds | 13.7% | 19.8% | +6.1 pp |

| Offshore | 1.3% | 1.6% | +0.3 pp |

| Quoted Equities | 20.7% | 9.4% | -11.3 pp |

| Immovable Property | 19.7% | 8.2% | -11.5 pp |

| Fixed Deposits | 2.7% | 2.8% | +0.1 pp |

| All other assets | 5.6% | 3.8% | -1.8 pp |

Two asset classes gained 24 percentage points of share. Two asset classes lost 23 percentage points of share. The map of Kenyan retirement wealth has been redrawn.

What changed

Three forces operated together over this period.

First, the Central Bank of Kenya raised policy rates aggressively from 2022 onward. Treasury bond yields rose into the high teens. Government paper became, for the first time in a decade, a genuinely competitive risk adjusted return. For a pension fund trustee with a fiduciary obligation to deliver returns at acceptable risk, the choice was almost made automatic.

Second, the Nairobi Securities Exchange struggled. Foreign investor outflows from 2022 to early 2024 left the market thin and falling. Most large cap Kenyan stocks ended 2024 below their 2018 levels in dollar terms. A pension fund that held NSE equities through this period earned negative real returns.

Third, public debt grew. Kenya's debt to GDP ratio rose from approximately 56 percent in 2018 to over 70 percent by 2024. The government issued a great deal of new domestic paper to fund itself. Pension funds were, by far, the largest single class of buyer.

Each of these forces independently nudged pensions toward government paper. Together they produced a structural reallocation rather than a tactical one.

The fiscal coupling

The mechanical implication is uncomfortable. With 54 percent of pension assets in government securities, the financial health of every contributing Kenyan worker is now directly tied to the financial health of the National Treasury. If the state services its debt comfortably, retirees do well. If the state restructures or defaults, retirees pay.

This is not a uniquely Kenyan situation. Most pension industries in emerging markets have meaningful sovereign exposure, and well run pension regulators set limits on it. The RBA caps single issuer concentration but does not cap sovereign concentration. The tacit assumption is that government paper is risk free. In an environment where the same state is also the regulator, the borrower, and the largest source of pension contribution policy, that assumption is worth examining.

What is more unusual is the speed of the shift. To move from 36 percent to 54 percent sovereign exposure in seven years is fast by any international comparison. It happened, in part, because the alternatives shrank. A struggling NSE, illiquid direct real estate, almost no functioning private credit market, an under developed alternatives sector. There was nowhere else to go that was both liquid and scaled.

What this means for the next decade

Three observations follow.

The first is structural. Without a deeper, more diversified Kenyan capital market, pensions will continue to crowd into government paper because that is where allocatable, liquid, scaled product exists. Building out alternatives, REITs, infrastructure bonds with credible structuring, and a deeper corporate bond market is now a pension industry imperative, not a nice to have. The pension money is there. The investable product is not.

The second is regulatory. The RBA may need to consider a soft cap on sovereign concentration, paired with incentives or carve outs for productive non sovereign asset classes. Without it, the trend continues mechanically. Trustees doing their job will keep buying T bonds.

The third is political. Pension money is no longer abstract savings. It is the most important domestic financing source for the Kenyan state. Decisions about debt management, fiscal consolidation, and any future debt restructuring are now also decisions about retirees. That makes them harder, more public, and more consequential. A pension regulator and a debt manager housed in the same government will eventually have to address that conflict openly.

The question

The Kenyan pension industry has done what it was set up to do. It has grown. It has diversified across asset classes, a little. It has avoided large losses. In the technical sense of fiduciary duty, it has performed.

The question the data raises is different. When more than half of every retirement shilling sits in the same place, and that place is the National Treasury, the pension industry has stopped being an investment system and has started being a financing system. For the state, that is convenient. For the worker who will retire in 2045 expecting their pension to pay out, the future depends entirely on what the state chooses to do between now and then.

Tags

Share this article